This article was written by Rupal Deshmukh, Partner and Suketu Gandhi, Chair, Strategic Operations. The original article was published by the Kearney. You can find the article here.

Outlooks brought to you by the Kearney Supply Chain Institute

The Supply Chain Navigator forecasts supply chain cost will rise in the range of 2.3 to 4.0 percent above inflation through 2026, driven by structural forces in trade policy, critical minerals constraints, geopolitical friction, and elevated inventory levels that persist even as container rates and commodity prices moderate.

These forces operate continuously and embed cost across supply chains between disruptions, creating a higher baseline that traditional cyclical indicators fail to capture.

Enterprise performance depends on how early this pressure is recognized upstream and how effectively it’s absorbed across planning, sourcing, and operations before options narrow and costs reset higher.

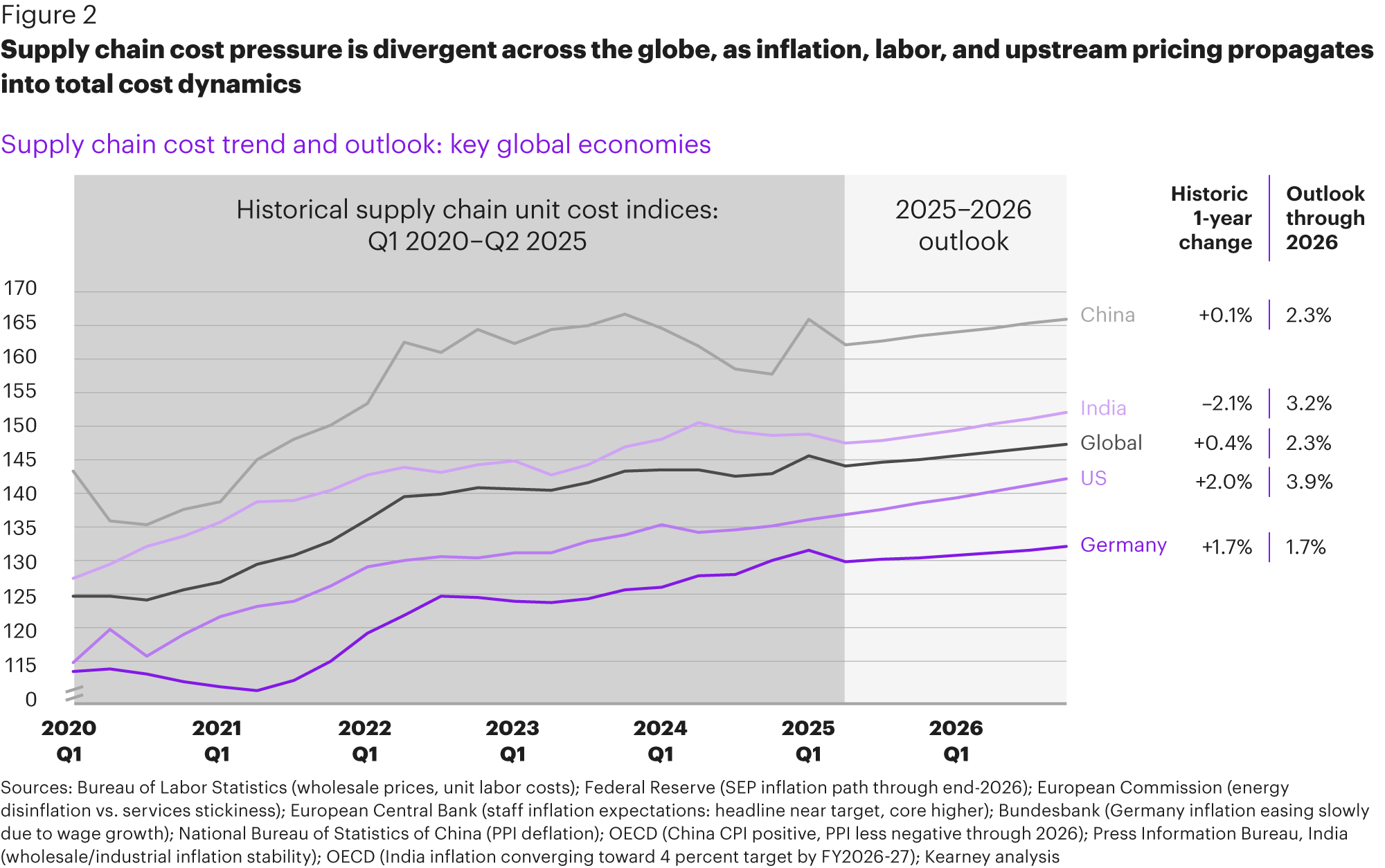

Supply chain costs are projected to rise 2.3 to 4.0 percent above baseline inflation through 2026, even as traditional indicators suggest stabilization.

Container rates have moderated from pandemic-era extremes, selected commodity inputs have declined sequentially, and inventory-to-sales ratios sit within historical ranges. These signals have encouraged expectations of broad-based cost normalization, but the Supply Chain Navigator forecast indicates otherwise (see figures 1 and 2).

The United States remains in a moderate inflation regime, with wholesale prices still rising and labor costs growing at low single-digit rates. Inflation is expected to move closer to target by the end of 2026.

In Europe, and particularly Germany, energy-driven disinflation continues while services inflation linked to wages remains elevated. Headline inflation is expected to trend near target in 2026, with underlying pressures easing only gradually.

China remains producer-price deflationary, supporting upstream cost relief while limiting pricing power. Consumer inflation is expected to stay positive, with producer prices improving only modestly through 2026.

India remains broadly stable, with mild wholesale and industrial inflation. Inflation is projected to converge gradually toward the 4 percent target through the end of 2026.

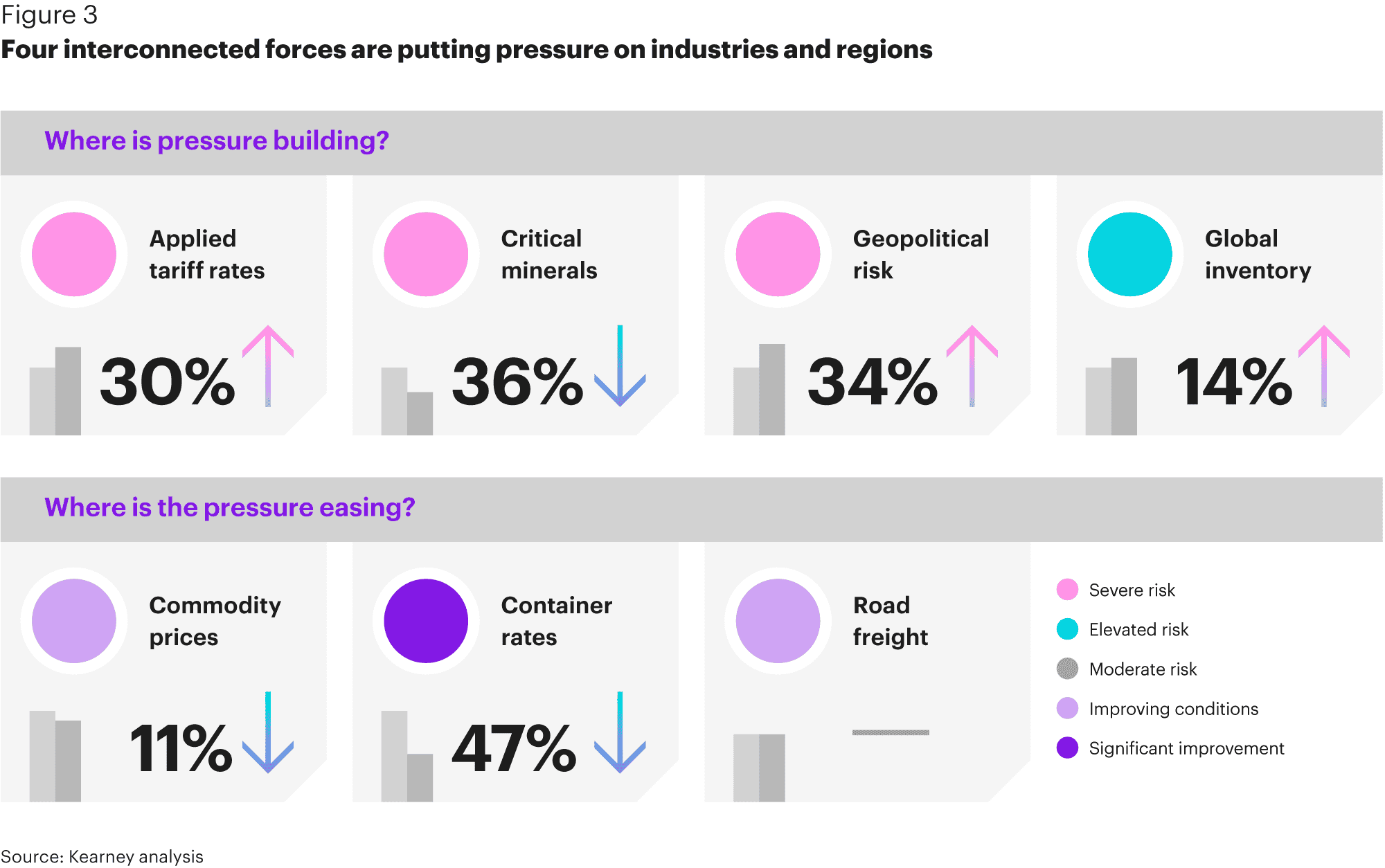

Four interconnected forces beyond the conventional drivers of supply chain costs are exerting sustained pressure across industries and regions: applied tariff rates, critical minerals exposure, geopolitical risk, and global inventory dynamics. These forces operate continuously, influence decisions well before their impacts manifest in operations, and contribute to the persistence of elevated supply chain costs even outside periods of disruption (see figure 3).

Across major economies, including China, Germany, the United States, and India, average tariff levels have risen by roughly 30 percent, driven by industrial policy, trade restrictions, and security considerations.

Tariffs have shifted from predictable trade friction to tools of geopolitical strategy, shaped as much by security and political considerations as by economic policy, creating cost pressure that persists even in the absence of formal policy changes.

Direct costs add up. Applied tariffs raise landed costs on affected goods—material and difficult to offset for organizations with large cross-border flows.

Policy uncertainty premiums compound. Organizations build inventory ahead of anticipated policy shifts, diversify supply bases, and structure contracts to manage tariff risk, increasing carrying costs and contractual complexity.

Tariffs embedded in planning. In earnings commentary and internal planning, manufacturers increasingly treat tariffs as part of the baseline cost structure, incorporating exposure directly into pricing decisions, cost baselines, and inventory valuation.

Compliance burden. Expanding trade controls, origin requirements, and reporting obligations add administrative cost that compounds in complex global networks.

Tariffs now operate as a standing cost in enterprise planning. Organizations that plan for them absorb pressure earlier.

Global exports of critical minerals have decreased by more than a third over the past year.

Analysis from the World Economic Forum supports this, noting that access to these materials is increasingly shaped by state control, export restrictions, and strategic stockpiling rather than by market-clearing mechanisms.

Concentration creates access risk. Processing capacity is concentrated in a small number of geographies where a single country often controls a large share of global refined output. Supply may remain available, yet access can be constrained by export controls, priority allocation, or price volatility driven by strategic considerations.

Volatility without interruption. Materials continue to move through established supply channels, while pricing increasingly reflects policy direction, geopolitical tensions, and long-term access security rather than near-term supply-and-demand conditions.

Exposure remains difficult to see. For many organizations, exposure exists in several tiers removed from subcomponents and production inputs that are not sourced directly. Exposure is often recognized only when cost, capacity, or delivery is already affected.

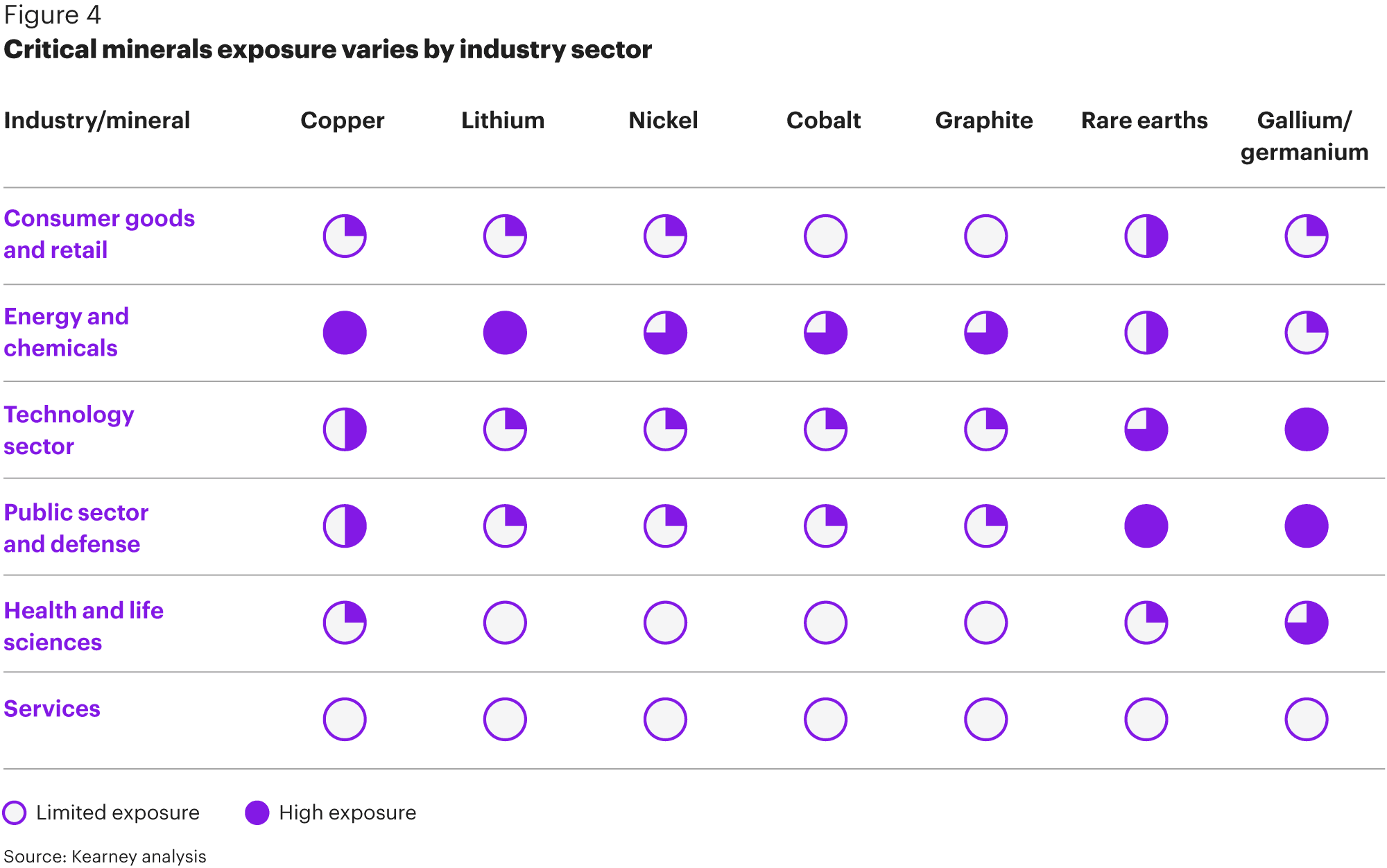

Demand drivers compound concentration. Electric vehicles, renewable energy, consumer electronics, and defense applications rely on many of the same critical minerals, concentrating demand pressure on a limited set of supply sources.

Figure 4 illustrates critical minerals exposure by industry sector. Energy and chemicals show high exposure across multiple material categories. Technology sectors show concentrated exposure to rare earths and specialized compounds. Industries with limited direct exposure, including consumer goods and healthcare, face indirect constraints through electronic components, packaging materials, or manufacturing equipment that depend on critical minerals several tiers upstream.

Limited visibility beyond first-tier suppliers increases the likelihood that access constraints translate into higher cost and reduced flexibility.

Heightened geopolitical risk—average risk index (GPRHC) across core global regions is up 34 percent in the past year—is shaping supply chain economics through persistent friction rather than visible disruption. Supply chains continue to operate, but efficiency declines, buffers increase, and costs rise.

Friction accumulates without shutdowns. Transportation routes lengthen as networks reroute around contested zones, adding time, distance, and fuel expense. Insurance premiums and risk surcharges rise across affected trade lanes, particularly for maritime shipments through regions with active conflict or elevated security threats. Financing costs increase as banks incorporate geopolitical risk into trade finance pricing and require additional collateral or documentation. Compliance requirements expand as sanctions regimes grow more complex and trade controls extend across products and geographies.

Regional effects travel through global networks. Geopolitical risk concentrates in specific regions such as contested maritime corridors, border crossings subject to policy volatility, or jurisdictions under sanctions. For example, a European manufacturer with no direct exposure to Asia can still face higher costs if Asian suppliers absorb higher financing costs or if capacity shifts toward regions with lower geopolitical risk.

Precautionary responses embed cost over time. Organizations respond through increased safety stock, duplicated capacity across geographies, and network designs favoring redundancy over efficiency—adding cost even when anticipated risks do not materialize.

Because operations continue, the impact is often treated as execution noise, delaying recognition and embedding cost over time.

Global inventory levels have risen by around 14 percent in the past year, with overstock more localized than global, and inventory pull-forward tied to trade policy timing.

Why inventory rises. Demand uncertainty increases safety stock. Trade policy uncertainty drives prebuild ahead of potential changes. Transportation reliability concerns add precautionary buffers. Longer planning horizons in a more complex geopolitical environment increase cycle stock.

Costs accumulate quietly. Higher inventory ties up capital, increases storage and financing costs, and faces greater risk of losing value before use. These costs accrue gradually, making them easy to overlook operationally.

Structural inventory embeds cost. Some inventory growth is tactical and unwinds as conditions stabilize. Other inventory reflects persistently higher uncertainty and embeds cost into day-to-day operations.

Inventory becomes one of the clearest ways in which uncertainty translates into sustained costs, reduced flexibility, and delayed responses across the enterprise.

Conditions are more stable than last year. Cyclical pressures have eased while structural forces persist, creating an opportunity for deliberate action rather than constant firefighting. Recent Kearney research shows that 70 percent of COOs predict 10 percent or greater revenue growth this year despite these structural pressures.

Supply chains are where this performance will be built or lost. And how organizations act now will determine whether pressure is absorbed through deliberate trade-offs or embedded into the operating baseline.

Across industries, organizations that navigate sustained cost pressures more effectively tend to exhibit several observable patterns.

Timing determines outcomes. Early recognition preserves flexibility in sourcing, inventory, and network configuration. Late recognition embeds cost through locked contracts, capacity commitments, and inventory positions.

Early signals often surface outside financial reporting, emerging instead in supplier behavior, logistics conditions, or constraints in sub-tier supplier networks. These signals are interpreted as early indicators of enterprise impact, not isolated operational noise.

During the Red Sea shipping crisis, early signals such as vessel rerouting, rising war risk insurance premiums, and extended transit times signaled mounting supply chain pressure weeks before most companies’ financials or service KPIs were affected. Enterprises that acted on these signals preserved flexibility in routing and capacity allocation that late responders lost.

Cost pressure compounds or dissipates based on how decisions connect across planning, sourcing, manufacturing, and delivery. Where decisions reinforce one another, trade-offs are managed early. Where they do not, cost becomes embedded over time.

When enterprises respond late to early signals, costs and complexity increase. Misalignment across planning assumptions, sourcing actions, and operational responses narrows options and accelerates cost embedding through inventory positions, capacity commitments, and service obligations.

Recent Kearney research highlights why alignment remains difficult, showing that while only one in three CFOs currently view procurement as a strategic partner, organizations that elevate procurement into enterprise decision-making are better positioned to align cost, risk, and trade-offs across the value chain.

Recognizing and acting on early signals places new demands on both technology and talent. The volume, speed, and interdependence of signals now exceed what experience and manual processes can manage on their own.

AI-enabled tools help surface patterns and test scenarios, enabling faster coordination across planning, sourcing, manufacturing, and delivery. Value emerges from earlier, more consistent decision-making across the performance chain, rather than from incremental efficiency gains.

Recent Kearney research shows that 94 percent of organizations have experimented with AI, and 50 percent are beginning to scale their implementations, with the most advanced progress in manufacturing and logistics. Organizations that move AI from isolated pilots to scaled production create an advantage through faster, more coordinated responses across the enterprise.

Talent remains central. Performance depends on whether leaders and teams have the skills to interpret signals, challenge assumptions, and act across functions with discipline. Technology expands visibility and speed, but outcomes are determined by how effectively judgment and coordination are applied.

These three patterns separate enterprises that absorb pressure strategically from those that embed it structurally. Early recognition, connected decisions, and coordinated capability determine whether cost pressure is managed or carried forward.

Supply chain costs will rise 2.3 to 4.0 percent above inflation through 2026, driven by structural forces in trade policy, critical minerals, geopolitics, and inventory. Enterprise performance now separates based on how early pressure is recognized upstream and how effectively decisions connect across planning, sourcing, and operations.